DP3 insurance is the dwelling fire policy many landlords use to protect a rental home with replacement cost coverage. It can pay to repair or rebuild after a covered loss, instead of cutting a check based on lower value after age and wear. Furthermore, many DP3 policies include fair rental value, which helps replace lost rent when the home is unlivable after a covered claim. Consequently, the policy you choose can decide whether a loss is a setback or a budget-breaker.

You've done the hard work. You found the deal, ran the numbers, closed, and placed a solid tenant. Therefore, the next job is keeping that cash-flow protected.

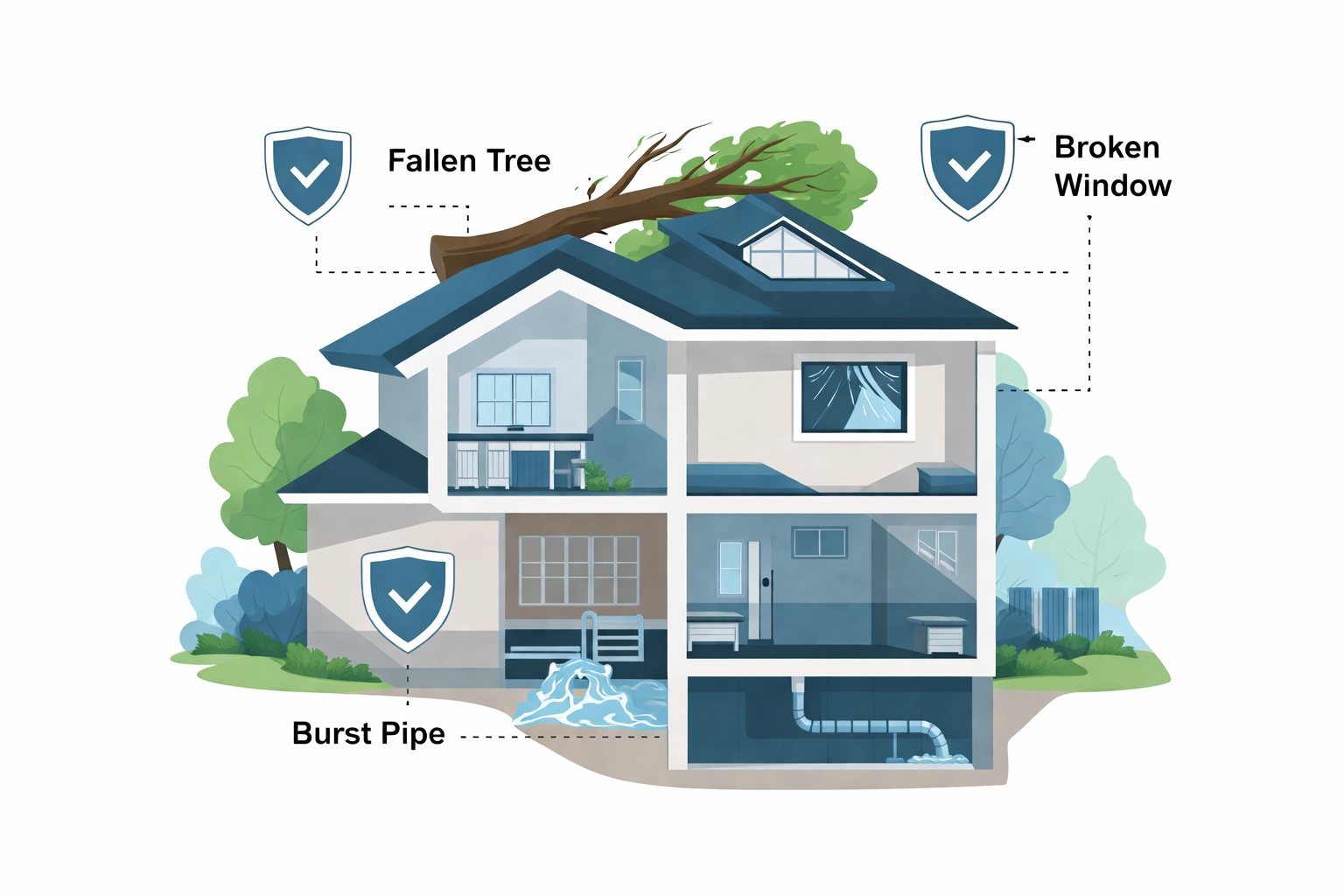

Then a pipe bursts. Or a tree crashes through the roof. Specifically, these are the losses that turn “good month” into “big repair bill.”

At that point, the insurance form matters. Consequently, if you still carry Actual Cash Value (ACV) coverage, the claim payment can come in far short when materials and labor spike.

Let’s break down DP3 insurance and why this dwelling fire policy is often the right fit for landlords who want tight, practical protection.

DP3 stands for Dwelling Policy Form 3. It’s a dwelling fire policy built for properties you don’t live in, such as rental homes, inherited properties, or vacation houses you rent out.

Think of it as the top tier of dwelling policies. DP1 and DP2 forms exist and can cost less. However, DP3 is usually the more complete option for many real estate investors.

The key difference is claim settlement. DP3 uses Replacement Cost Value (RCV) for the dwelling. Consequently, after a covered loss, you can get paid to fix or rebuild, not a lower value amount that forces you to cover the gap.

This is where many investors get caught. Therefore, keep it simple.

Actual Cash Value (ACV) pays what the damaged item is worth today. It includes age, wear, and depreciation. For example, a 15-year-old roof gets destroyed by a storm. Consequently, ACV may pay only 40–60% of the replacement cost because the roof is “old.”

Replacement Cost Value (RCV) pays what it costs to repair or replace with something similar. Same roof, same storm. Therefore, the payment can cover the full replacement cost.

Here’s a quick example that shows the gap:

| Scenario | ACV Payout | RCV Payout |

|---|---|---|

| 15-year-old roof destroyed | ~$6,000 | ~$15,000 |

| HVAC system failure | ~$2,500 | ~$7,000 |

| Fire damage to kitchen | ~$18,000 | ~$35,000 |

See the pattern? With ACV, you often pay the difference out of pocket. With RCV on a DP3 policy, the payout tracks what repairs cost in today’s market.

For long-term landlords, this is not a minor detail. Consequently, it can shape your returns for years.

Here’s another reason DP3 is often the smarter choice for real estate investors.

DP3 is an open peril policy for the dwelling. Therefore, it covers direct physical loss unless the policy excludes it. Flood is excluded, so you need separate flood insurance. Earthquake is usually excluded as well. Consequently, you get broad protection without guessing which “named peril” applies.

Compare that to DP1, which only covers nine named perils:

If your loss doesn't fit neatly into one of those boxes? Tough luck.

With DP3, coverage often applies to losses like:

Consequently, open peril coverage can mean fewer surprises at claim time. You spend less time arguing over whether your loss fits a narrow list.

Say a fire damages the rental so badly your tenants must move out during repairs. That is not only a repair bill. Consequently, it can also mean months of lost rent.

DP3 policies typically include Fair Rental Value coverage (often called Coverage D). Therefore, it can help replace lost rent while the property is unlivable due to a covered loss.

Your mortgage doesn't pause because of a kitchen fire. Your property taxes don't care that a tree fell through the living room. This coverage keeps cash flowing when your property can't.

For investors carrying multiple rentals, this protection alone can justify the premium difference between DP3 and cheaper alternatives.

Not every property needs the same coverage level. However, DP3 is often the right call when:

✅ Long-term rentals are your plan – Consequently, the RCV benefit matters more as the property ages

✅ Older buildings are in your mix – Therefore, depreciation can crush ACV payouts

✅ You’re building a buy-and-hold portfolio – Specifically, strong coverage keeps you in the game

✅ Major upgrades are in the home – Furthermore, ACV may not match what you’ve put in

✅ Big out-of-pocket bills would hurt – Consequently, a large claim gap can strain cash flow

Even with DP3, mistakes still happen. Therefore, watch for these:

🚫 Underinsuring the dwelling – A $150,000 limit will not rebuild a $225,000 home. Consequently, you still eat the gap. Set limits based on real replacement cost.

🚫 Skipping liability coverage – DP3 mainly addresses property damage. However, liability still matters. A guest slips on stairs. Therefore, you could be facing a lawsuit.

🚫 Missing other structures – Detached garages, sheds, and fences need coverage, too. Specifically, confirm how Coverage B is set.

🚫 Thinking tenants are covered – The policy protects the building and your rental income. Consequently, tenant belongings are not included. Require renters insurance.

🚫 Not reviewing each year – Construction costs rise. Values shift. Therefore, last year’s limit can leave you short today.

For more on avoiding coverage gaps, check out The Do's and Don'ts of Insuring Your Residential Investment Property.

Quick sidebar for investors who might be tempted to just keep their homeowners policy on a property they've converted to a rental: don't.

Standard homeowners insurance (HO3) is designed for owner-occupied properties. The moment you rent that property out and stop living there, you've likely violated your policy terms. If you file a claim, the carrier can deny it based on occupancy status alone.

A dwelling fire policy like DP3 is specifically built for non-owner-occupied properties. It's the right tool for the job.

We covered this in detail here: Why a Standard Homeowners Policy Can Leave Real Estate Investors Exposed.

DP3 insurance is not the cheapest option. However, for investors building a rental portfolio, it is often the cleanest way to avoid big coverage gaps.

Replacement Cost Value means you are not funding part of your own claim. Furthermore, open peril coverage helps close common holes. Consequently, fair rental value coverage can keep income coming in after a covered loss.

At RealAssure, we specialize in residential investor insurance programs built specifically for landlords and portfolio owners. We understand that your rental properties are investments: not just buildings: and we structure coverage accordingly.

Ready to make sure your rentals are actually protected? Get a quote and see what proper coverage looks like for your portfolio.