Your roof just took a beating from last month's hailstorm. You're looking at $15,000 in repairs. The question keeping you up at night: should you file that insurance claim?

For landlords with DP3 policies, roof claims are a double-edged sword. Yes, that's why you pay premiums. But one claim could trigger rate increases that cost you thousands more over the next 3-7 years. And if your roof is already aging? You might be facing policy non-renewals or forced coverage downgrades.

Here's what every residential investor needs to understand about roof claims and dwelling fire policy rates.

A first roof claim typically increases your DP3 insurance premiums by 7-10%. That might sound manageable: until you do the math.

If you're paying $2,000 annually for landlord insurance, a 10% hike means an extra $200 per year. Over five years (the typical claims history window), that's $1,000 in additional costs. For a repair that might have cost $3,000 out of pocket.

The numbers get worse with multiple claims. A second claim within a few years can push your premiums up 25-40%. A third claim? Some carriers will simply non-renew your policy, forcing you into the non-standard market where rates can double.

The impact timeline varies by carrier:

Your claims history follows you. Even if you switch insurers, most carriers pull loss history reports that show every claim filed in the past 5-7 years.

Here's a critical distinction that most landlords miss: insurance companies treat different types of roof damage very differently.

Storm-related claims (hail, wind, hurricane damage) are classified as "acts of God." Because these events are beyond your control, insurers typically assess minimal rate increases: especially in areas prone to severe weather. A hail claim in Texas or a wind claim in Florida won't hammer your rates as hard as other claim types.

Non-weather damage tells a different story. Fire damage to a roof can trigger premium increases of 30% or more. Why? Insurers view these as potential indicators of higher risk or negligence. The same applies to roof damage from falling trees that weren't properly maintained or structural issues that suggest deferred maintenance.

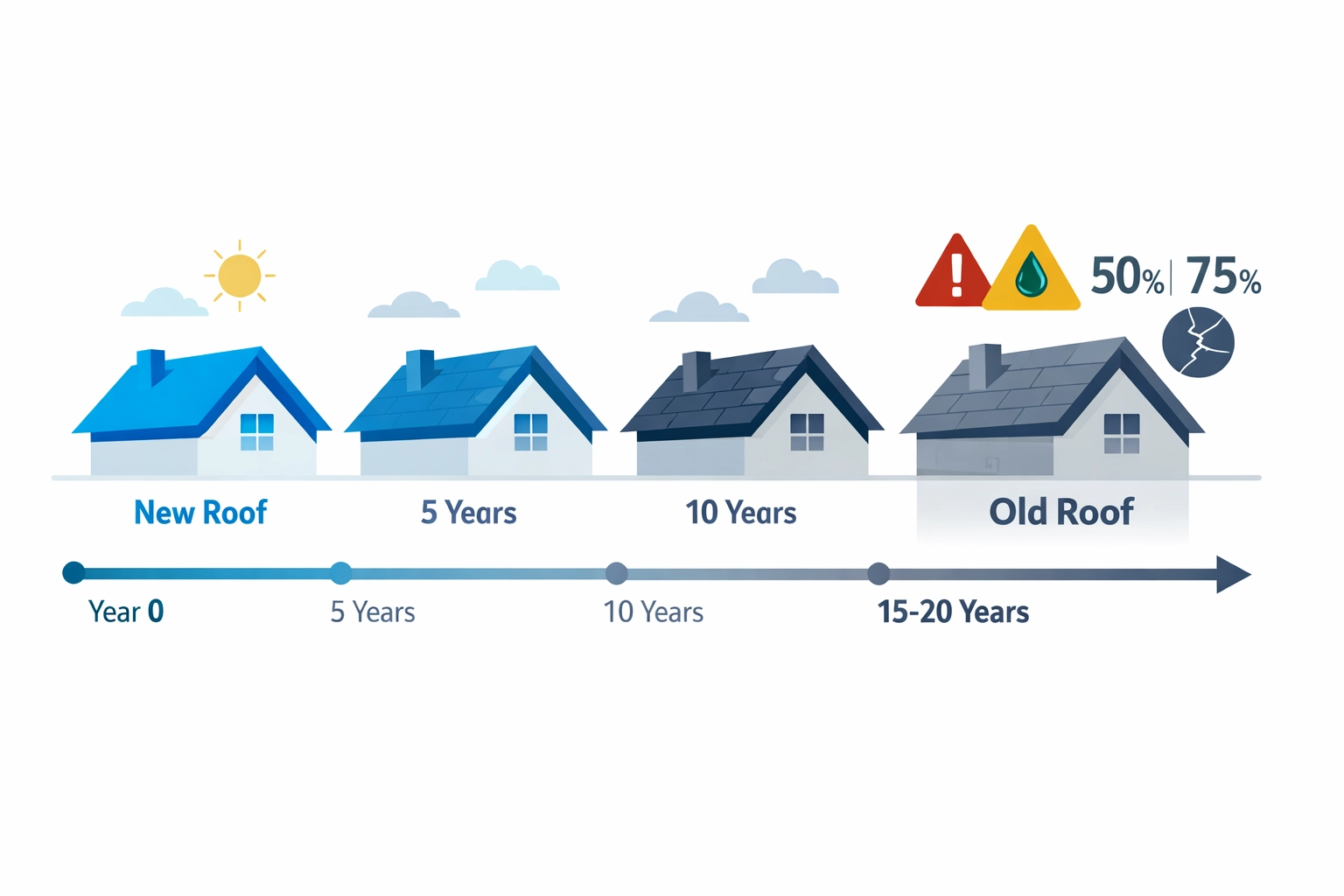

Even without claims, your roof's age is quietly eroding your insurance coverage and inflating your costs.

Most insurance carriers implementing age-based restrictions at the 15-year mark. Once your roof crosses this threshold, expect these changes:

Wind and hail deductibles double from 1% to 2% of dwelling value. On a $300,000 rental property, your deductible jumps from $3,000 to $6,000.

Coverage switches from RCV to ACV for roofs 15-20 years old. This shift can cut your claim payout by 50% or more (more on this below).

Some carriers refuse to write new policies on properties with roofs older than 15 years. If you're buying an investment property with an aging roof, you might face limited insurance options and higher premiums from day one.

For roofs over 20 years old, many carriers require a professional roof inspection before binding coverage. If the inspector finds any deficiencies, you'll need to replace the roof before obtaining insurance for real estate investors.

This is where landlords lose thousands of dollars without realizing it until claim time.

Replacement Cost Value (RCV) pays the full cost to replace your roof with new materials, minus your deductible. If your 10-year-old roof needs replacing and the cost is $25,000, you receive $25,000 (minus deductible).

Actual Cash Value (ACV) pays replacement cost minus depreciation. That same $25,000 roof replacement might only net you $12,500 after the insurer applies 50% depreciation for a 10-year-old roof.

Most DP3 policies default to RCV coverage when roofs are newer. But carriers automatically switch to ACV once roofs hit certain age thresholds: often without explicitly notifying you beyond the fine print in your renewal documents.

Here's the depreciation reality:

Check your dwelling fire policy declarations page right now. If your roof is over 10 years old and your policy doesn't explicitly state "RCV for roof," you're likely on ACV coverage.

Your insurance carrier isn't just evaluating claims. They're monitoring the overall condition of insured properties: especially roofs.

Carriers now use aerial imagery and drone technology to assess roof conditions without ever stepping on your property. They're looking for:

If their assessment flags issues, you'll receive a notice requiring repairs within 30-90 days. Ignore it, and your policy won't renew.

Document everything. Keep receipts for all roof maintenance and repairs. If a carrier questions your roof's condition, photographic evidence and contractor invoices prove you're maintaining the property.

Annual roof inspections by licensed contractors cost $150-300 but can prevent coverage cancellations. Many insurers offer small premium credits (2-5%) for properties with documented annual maintenance.

Smart landlords approach roof issues strategically, not reactively.

Run the break-even analysis before filing. If repairs cost less than 2-3 times your deductible, pay out of pocket. The long-term premium increases often exceed the immediate claim payout.

Time roof replacements strategically. If your roof is 12-14 years old and showing wear, replace it before it hits 15 years. A new roof can reduce premiums by 5-35%, and you'll secure RCV coverage for the next 15 years.

Consider impact-resistant shingles. These qualify for insurance discounts of 5-15% in most states and significantly reduce future hail damage claims. The upfront cost premium pays for itself in 4-7 years through lower premiums.

Ask about claim forgiveness programs. Some carriers offer first-claim forgiveness, especially for long-term customers with otherwise clean records. This perk isn't advertised: you need to ask your agent.

Review your policy annually. Don't wait for renewal. Schedule a mid-term policy review to verify your roof coverage type (RCV vs. ACV), confirm your deductibles, and discuss any property improvements.

For residential investors holding multiple properties, consider which properties warrant comprehensive coverage versus basic protection. Your newest acquisitions with newer roofs deserve DP3 policies with full RCV coverage. Older properties with aging roofs might be candidates for ACV policies with lower premiums: since you'd likely replace rather than repair anyway.

Roof claims don't automatically destroy your landlord insurance rates, but they demand careful consideration. A single claim can cost you thousands in premium increases over 5-7 years. Multiple claims can make you uninsurable in the standard market.

Your roof's age matters as much as claims history. Once a roof crosses 15 years, carriers restrict coverage and increase costs: whether you've filed claims or not.

The smartest move? Proactive maintenance and strategic roof replacement before age-based restrictions kick in. A $10,000 roof replacement today beats $20,000 in cumulative premium increases and reduced coverage over the next decade.

Need help evaluating your current DP3 insurance coverage or comparing options for properties with aging roofs? Get a quote from RealAssure: we specialize in insurance for real estate investors who need coverage that actually protects their investment returns.

{kind=link}