Shopping for REI insurance in Broward County feels like navigating a maze blindfolded. One agent tells you to buy a DP3 policy, another pushes builder's risk, and Google results just confuse you more. Meanwhile, your rental property sits there unprotected, or worse, covered by the wrong policy entirely.

Here's the truth: residential real estate investors need specialized coverage that standard homeowners policies simply don't provide. Whether you own a single fix-and-flip in Pompano Beach or manage five short-term rentals across Fort Lauderdale, these 10 essentials will help you avoid costly gaps in your protection.

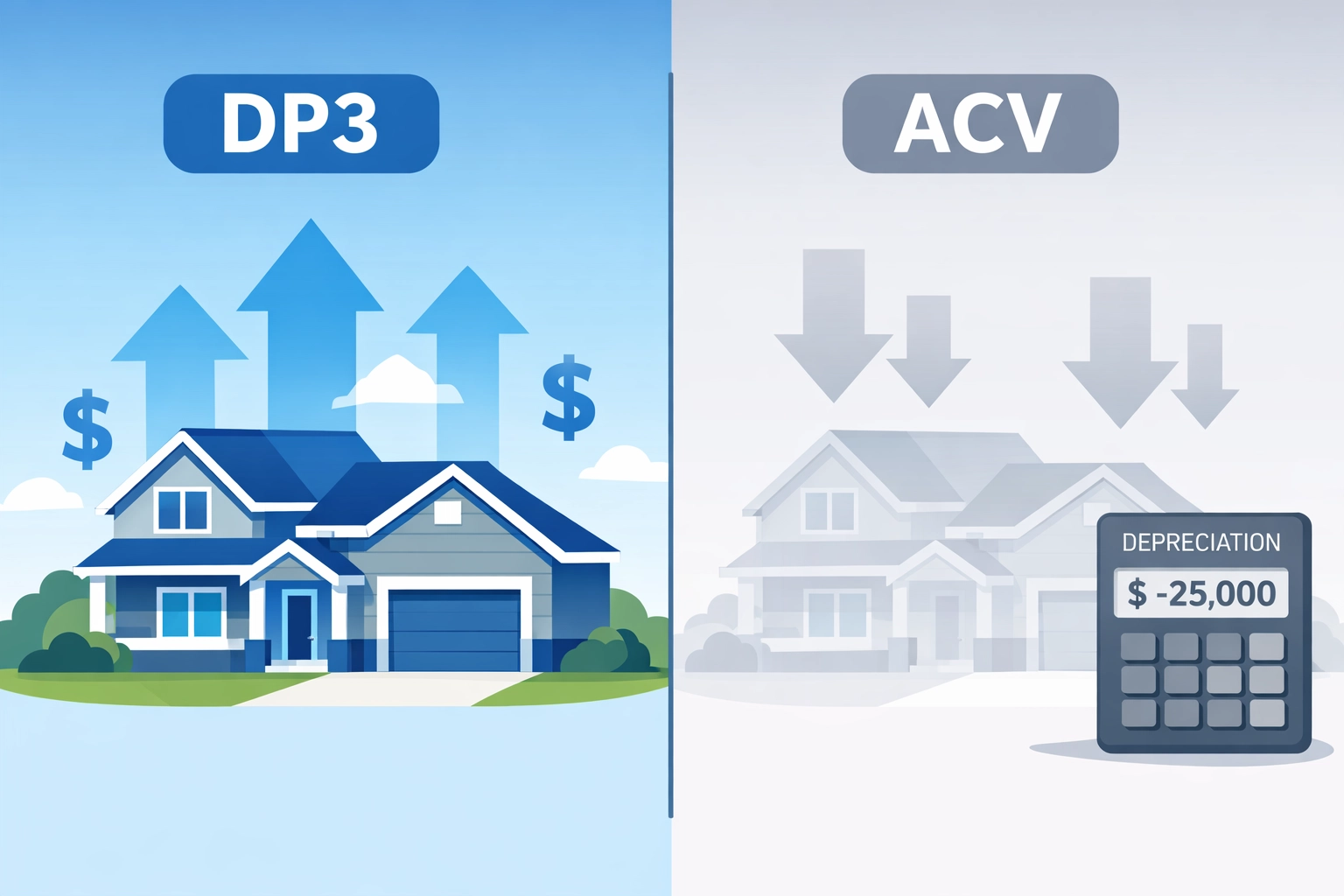

A DP3 (Dwelling Fire) policy pays to rebuild your property at today's construction costs. If a fire destroys your $300,000 rental, you get $300,000 to rebuild, straightforward protection that keeps your investment intact.

Actual Cash Value (ACV) policies work differently. These policies subtract depreciation from your payout. That same $300,000 rental might only receive $180,000 after factoring in age and wear. You're stuck covering the $120,000 gap out of pocket.

For residential investors, DP3 policies make financial sense. Your rental property is a revenue-generating asset, not just a place to live. Replacement cost coverage ensures one catastrophic event doesn't derail your entire investment strategy.

Confusion between these two policies costs investors thousands every year. Builder's risk insurance protects properties undergoing active construction or major renovation. Your crew is on-site, materials are being delivered, and work is progressing. This policy covers theft of materials, vandalism during construction, and damage from weather events.

Vacant property insurance applies when a building sits empty with no active work happening. Maybe you're marketing it for sale, or tenants just moved out and you haven't found replacements yet. Standard policies often exclude vacant properties after 30-60 days, leaving you completely exposed.

Here's the deciding factor: Is someone actively working on the property? If yes, you need builder's risk. If no, vacant property insurance fills the gap. We've covered this distinction in detail for investors managing rehab projects.

Running an Airbnb or VRBO in Broward County creates liability exposures that traditional landlord policies don't address. Guests are considered "invitees" rather than tenants, which changes your legal responsibility dramatically.

Standard DP3 policies typically exclude short-term rental activity. If a guest slips on your pool deck or claims food poisoning from your welcome basket, your policy might deny the claim entirely. You're personally liable for medical bills, legal fees, and potential settlements.

Additionally, short-term rental liability insurance covers property damage caused by guests. That broken sliding glass door or stained carpet becomes your problem without proper coverage. For Florida investors capitalizing on tourism markets like Fort Lauderdale Beach, specialized STR coverage isn't optional: it's essential protection for your business model.

Most residential investors depend on rental income to cover mortgages, taxes, and operating expenses. When a hurricane forces your property to sit vacant for three months during repairs, those expenses don't disappear.

Loss of rent coverage (also called rental income protection) reimburses you for lost rental income during covered repair periods. If your property normally generates $2,500 monthly and repairs take four months, you receive $10,000 to cover your carrying costs.

This coverage kicks in only when a covered peril makes the property uninhabitable. Routine vacancies between tenants don't qualify. However, for serious damage from fires, storms, or water intrusion, this protection preserves your investment's cash flow exactly when you need it most.

You don't need a massive portfolio to face devastating lawsuits. A single slip-and-fall claim can generate six-figure medical bills and legal expenses that exceed your property's value.

General liability coverage defends you when tenants, guests, or contractors are injured on your property. Someone trips on uneven pavement in your parking area. A tenant's child is injured on a defective playground structure. Your property manager gets bitten by a tenant's dog during an inspection.

Without liability coverage, you're paying attorneys out of pocket while potential judgments threaten your personal assets. Most policies provide $1-2 million in protection, creating a barrier between claims and your savings accounts. For small landlords managing 1-4 properties, this coverage costs a few hundred dollars annually: a negligible expense compared to lawsuit exposure.

Managing five separate insurance policies for five properties creates administrative headaches and leaves money on the table. Portfolio policies (also called blanket policies) consolidate multiple properties under one master policy.

Benefits multiply as your holdings grow. First, you eliminate redundant paperwork: one renewal date, one payment, one point of contact. Second, you typically receive volume discounts that reduce per-property costs by 15-25%. Third, coverage often includes automatic protection for new acquisitions up to a certain value, eliminating gaps during transitions.

Portfolio policies work best for investors with 5+ properties in similar markets. If you own eight rentals across Broward and Palm Beach counties, consolidating them creates efficiency while improving your coverage consistency. This approach scales with your business rather than forcing you to juggle multiple carriers and renewal schedules.

Many investors mistakenly believe their policy covers tenant negligence. It doesn't. Your REI insurance protects the building and your liability as the property owner. Tenant belongings and tenant-caused damage require different handling.

Landlord liability covers injuries or damages resulting from your negligence: like failing to repair known hazards or maintaining unsafe conditions. Your policy responds to these claims because they stem from your responsibilities as the property owner.

Tenant liability involves damages caused by tenant actions or negligence. A tenant leaves the faucet running and floods three units. Their friend is injured during an unauthorized party. These situations fall under the tenant's responsibility.

Smart investors require tenants to carry renters insurance and include this requirement in lease agreements. This creates a clear liability boundary and ensures tenant negligence claims don't become your financial problem. However, your policy still needs robust liability limits because courts often pursue landlords regardless of fault.

Condo and townhouse investors face unique insurance situations because of HOA master policies. These association-level policies cover common areas and building exteriors, but they don't eliminate your need for individual coverage.

HOA master policies typically fall into two categories. "Bare walls" policies cover only the building structure itself: you're responsible for everything inside your unit walls. "All-in" policies extend coverage to original fixtures and installations, but your upgrades and personal property still require individual coverage.

Additionally, master policies often carry high deductibles ($5,000-$25,000 per occurrence) that the association may pass through to responsible unit owners. If a pipe burst in your unit floods three others, you could face substantial assessment charges without proper coverage.

Your individual condo policy fills gaps in the master policy, covers your improvements and betterments, protects your rental income, and provides liability coverage for incidents in your unit. For Broward County investors buying coastal condos, understanding this coverage layering prevents nasty surprises after claims.

Homeowners policies are designed for owner-occupied residences, not investment properties. Using one for your rental creates dangerous coverage gaps that insurers exploit during claims.

Standard homeowners policies exclude business activities: and renting property qualifies as business activity. They limit liability for non-resident injuries. They don't cover lost rental income. They may deny claims entirely if they discover the property isn't owner-occupied.

Specialized REI insurance addresses investment-specific risks. Coverage includes rental income protection, higher liability limits for tenant-related claims, protection during vacancy periods, and coverage that acknowledges the property's business use. These policies cost slightly more than homeowners insurance, but they actually pay claims when you need them.

Florida's insurance market is unlike anywhere else in the country. Wind and hurricane exposure, flood zone requirements, and the state's litigation environment create complexity that generic national agents simply don't navigate well.

A local REI insurance specialist brings specific advantages. They understand which carriers actually write policies in Broward County versus which ones have pulled out of the market. They know how to structure coverage to satisfy lender requirements while minimizing Citizens assignments. They can explain the differences between named storm deductibles and hurricane deductibles in plain English.

Additionally, coastal properties require flood insurance through the National Flood Insurance Program (NFIP) or private flood carriers. Local specialists help you determine correct flood zones, explain base flood elevation requirements, and coordinate wind/flood coverage so you're not paying twice for the same protection.

For residential investors building portfolios in Fort Lauderdale, Hollywood, or Pembroke Pines, working with someone who lives and breathes Florida's insurance challenges makes the difference between proper protection and expensive mistakes.

REI insurance isn't something you figure out after a claim gets denied. These 10 essentials create the foundation for proper protection, whether you own one rental or fifteen.

Your residential investment properties deserve coverage designed for their specific risks. Standard policies leave you exposed, while specialized REI insurance protects both your assets and your income stream. Additionally, working with local specialists who understand Florida's market ensures you're not navigating these complexities alone.

The difference between adequate coverage and devastating gaps often comes down to understanding these fundamentals before you need to file a claim.